Gold ETF marketing in India sells a single number: the expense ratio. It is usually a tidy 0.40% to 0.50%, and it looks cheap. The problem is that number is the visible tip of a much larger cost stack.

Brokerage, demat account maintenance charges, GST on every trade, and the impact cost of executing in a thinly traded counter all sit below the waterline. The real annual cost, including brokerage, demat AMC, GST, and impact cost, can exceed 1.5% [verify against specific trade data].

Fund houses have no incentive to show you that math.

| Key Takeaways • Gold ETFs provide exposure to gold without the storage, security, and purity concerns associated with physical gold. • When comparing Gold ETFs, look beyond the expense ratio. Tracking error, liquidity, trading volume, and bid-ask spreads can also affect investor returns. • Investors should compare a fund’s historical performance with domestic gold price movements to understand how closely it tracks the underlying asset. • Sovereign Gold Bonds have historically offered additional benefits for long-term investors, but availability depends on government issuance schedules. • Physical gold, Gold ETFs, and Sovereign Gold Bonds each have different advantages. The best choice depends on your investment horizon, liquidity needs, and personal preferences. • Before investing, review the latest factsheets, expense ratios, and fund disclosures, as costs and fund characteristics can change over time. |

The confusion runs deeper. Sovereign Gold Bonds, the tax-efficient darling, are paused with no clarity on when the government will resume issuance.

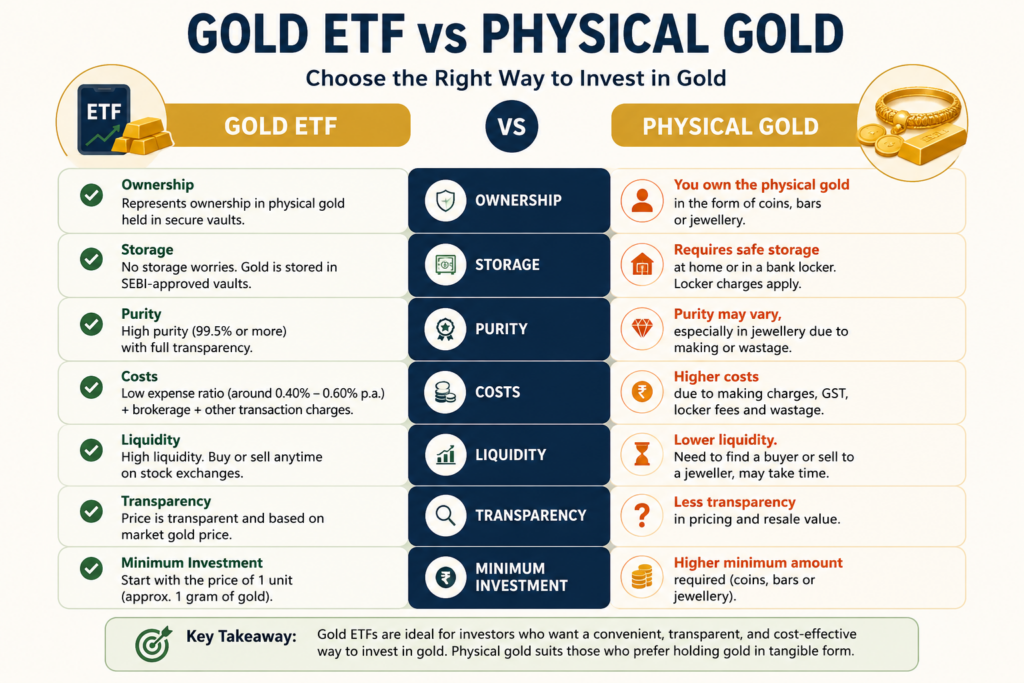

Digital gold platforms operate in a regulatory grey zone with no statutory backing for investor claims. Physical gold carries making charges, purity risk, and locker fees that compound over decades.

Every option leaks value somewhere.

The Indian saver who simply wants gold exposure without emotional loss, the jewellery that sits in a locker but never gets sold, is left paralysed by half-truths.

This guide is a fiduciary audit, not a product pitch. It equips you to calculate your own total cost of ownership across every gold vehicle available to an Indian resident. We reframe ETF allocation for a specific cultural need: liquidity without the emotional severance of selling family gold. The numbers will surprise you.

| Why Liquidity Matters A Gold ETF’s expense ratio is only one part of the overall cost of investing. Liquidity also matters. ETFs with lower trading volumes may have wider bid-ask spreads, which can increase the effective cost of buying or selling units. For this reason, investors often compare trading volume and spreads alongside expense ratios when selecting a Gold ETF. Using limit orders instead of market orders can also help reduce execution costs. |

Before you can measure the cost, you need to understand the structure. Let’s dismantle what a Gold ETF unit actually represents.

Custody, Purity, and Insurance: Where Your Gold Actually Sits

The gold backing your units is not a book entry. It is physical metal, 99.5% purity or higher, held in a SEBI-approved vault under a tripartite agreement between the fund house, the custodian (a scheduled bank), and the trustee.

The trustee, an independent entity, oversees the custodian and ensures the gold exists and is segregated from the custodian’s own assets. This structure means that even if the fund house fails, the gold remains in the trust, ring-fenced for unit holders.

SEBI mandates an independent auditor to physically verify the gold at least twice a year. The auditor checks bar counts, serial numbers, and purity against the custodian’s records.

The reports are filed with SEBI and are publicly accessible. You can, in theory, trace your fractional claim to a specific set of audited bars.

This is a regulatory fact, not a marketing claim.

The gold is insured against theft, damage, and custodian insolvency. The insurance cost, along with vaulting and audit fees, is embedded in the expense ratio.

You do not receive a separate custody bill. Compare this to a personal bank locker: you pay annual rent, arrange your own insurance, and bear the risk of loss without independent audit.

The ETF’s custody chain is more robust and more transparent than any individual arrangement.

Gold ETFs vs. Gold Funds of Funds: Clearing the Confusion

A Gold Fund of Funds (FoF) is a mutual fund scheme that invests in units of an underlying Gold ETF. It does not hold physical gold directly.

When you buy a Gold FoF, you are buying units of a mutual fund, not an exchange-traded instrument. The FoF settles at a single end-of-day NAV, and you cannot exit intraday.

If gold spikes at 11 a.m. and collapses by 3 p.m., the FoF investor is locked in until the day’s close.

The ETF investor can sell into the spike.

The FoF adds a second layer of expense ratio. The underlying ETF charges its own expense ratio, and the FoF charges an additional management fee on top.

This double-dip drags returns. A Gold ETF with a 0.50% expense ratio, when held through a FoF charging 0.25%, delivers a combined cost of roughly 0.75% before any other charges.

Over a decade, that extra 0.25% compounds into a meaningful erosion of your gold exposure.

The FoF’s one advantage is that it does not require a demat account. You can buy and sell through a regular mutual fund platform or directly with the fund house.

For an investor who cannot or will not open a demat account, the FoF is a workable, if costlier, access point. But if you already hold stocks or ETFs in a demat account, the direct ETF route is structurally cheaper and gives you real-time control.

The choice is not about which product is “better” in the abstract.

It is about whether you are willing to pay an ongoing fee to avoid a one-time demat account setup.

With the structure clear, the next question is practical: how do you actually buy these units on an Indian exchange without getting burned by a wide spread?

How to Buy Gold ETFs in India: From KYC to Execution

Knowing what a Gold ETF is doesn’t help if you can’t execute a trade without getting burned by a wide spread. The mechanics look simple on paper. The friction points (demat charges, thin liquidity, and the absence of SIPs) hide real costs. This section maps the purchase process with those friction points in sharp focus.

Prerequisites: Demat, Trading Account, and KYC

You need two accounts to buy Gold ETFs directly. A demat account holds the units. Your trading account places orders on the NSE or BSE. Most full-service brokers (Zerodha, Angel One, ICICI Direct) bundle both during account opening. KYC is the standard PAN-based process you completed for mutual funds.

The cost that fund factsheets never mention is the demat annual maintenance charge (AMC). For a small gold allocation (say, ₹50,000 to ₹1 lakh), a ₹300–₹500 yearly AMC [verify against your broker’s latest tariff] silently erodes roughly 0.3–0.5% of your holding value every year.

That drag compounds. It is entirely absent from the ETF’s expense ratio. If your gold exposure is modest, this single line item can make the ETF more expensive than physical gold held in a locker.

Placing Orders: Limit Orders vs. Market Orders on NSE/BSE

Log into your trading terminal. Search for the ticker (GOLDBEES, AXISGOLD, or HDFCGOLD) and pull up the market depth window before you touch the buy button. You will see a bid-ask spread: the gap between the highest price someone is willing to pay and the lowest price someone is willing to sell.

| Before buying a Gold ETF, it is worth checking the bid-ask spread and trading volume. ETFs with higher liquidity generally have tighter spreads, which can help reduce trading costs. Using a limit order instead of a market order can also help you avoid paying more than expected during execution. |

A market order in a Gold ETF is a rookie mistake. Thin liquidity means your order will sweep the order book. You eat through multiple price levels and deliver immediate slippage to yourself. You will pay more than the on-screen price. The spread you cross is a real cost that no TER captures.

Limit orders are non-negotiable. Set your price at or inside the best bid-ask, and wait.

Patience is the cheapest execution tool you have.

The Demat-Free Pathway: Using Gold ETF Fund of Funds

If you don’t have a demat account and don’t want one, Gold FoFs offer a familiar mutual fund wrapper. You buy units directly from the fund house or through platforms like Groww or Kuvera, just like any other scheme. No demat,no trading account, no AMC.

The trade-off is a second layer of costs. The FoF charges its own expense ratio, typically [verify against specific scheme documents], on top of the underlying ETF’s TER. Combined, the total annual cost can approach or exceed 1%, which is higher than a direct ETF held in a demat account for a large enough holding.

For small allocations, though, the demat AMC avoidance can tip the math in the FoF’s favour. You have to run the numbers for your specific amount.

Systematic Accumulation Without Timing the Market

Direct Gold ETFs do not offer SIP mandates. There is no automated monthly debit and unit purchase. If you want to accumulate gold systematically, you must log in each month, check the spread, place a limit order, and execute manually. Most investors won’t do that with discipline.

FoFs solve this by design. They accept SIPs, making rupee-cost averaging effortless. For a volatile asset like gold, averaging your entry price across cycles matters far more than shaving a few basis points of cost. The FoF’s higher expense ratio is often the price of behavioural consistency.

That is a trade worth making if the alternative is sporadic, ill-timed lump sums.

But before you place that first order, you need to decide whether a Gold ETF is even the right instrument. The comparison ahead is the most important decision matrix in this guide.

The Hidden Costs of Digital Gold Platforms

Digital gold platforms market themselves as the frictionless, “₹1 se shuru” entry point. What they bury is the spread. Every buy and sell transaction embeds a 2–5% gap between the price you pay and the price you would receive if you sold immediately.

Add GST on the purchase leg, and you are down 3–7% before the gold price moves a rupee. There is no exchange-traded liquidity: you sell back to the platform at its price. And the regulatory ambiguity is real. These wallet-based offerings sit outside SEBI’s mutual fund framework and outside RBI’s sovereign guarantee.

You are trusting a private entity’s vaulting and its promise to honour redemptions. For a serious allocation, that is an unnecessary risk.

The buyback spread on physical gold jewellery can exceed 10%, contrast with an ETF bid-ask spread that is often a few paise per unit for a liquid fund. That gap alone erases years of gold price appreciation.

If the matrix points you toward Gold ETFs, the next question is not “which fund?”, it’s “what will this actually cost me?”

Cost is only one side of the risk equation. The benefits are real, but so are the risks the marketing brochures omit.

Benefits and Risks: What the Marketing Brochures Omit

Every Gold ETF advertisement sells you liquidity, transparency, and safety. None of them mention tracking error, currency risk, or what happens when you try to exit a thinly traded counter on a volatile day. The benefits are real, but they come with conditions that fund houses prefer you skip.

The Real Benefits: Liquidity, Transparency, and No Locker Anxiety

You can sell a Gold ETF unit during market hours and receive the proceeds by the next trading day. That intraday exit capability is genuine. It means you don’t wait for a jeweller’s quote or a bank’s buyback window.

SEBI mandates daily NAV disclosure and a public portfolio file showing every gram of gold the fund holds. You know exactly what backs your units. No purity test, no making-charge loss, and no locker rent at the investor level. The fund bears custody and insurance, not you.

But intraday liquidity is only as good as the counter you pick. In a low-volume ETF, your sell order can sit while the price drifts against you. The benefit exists on paper; in practice, it belongs to the handful of ETFs that trade in meaningful size every day.

Market Risk, Currency Risk, and the Inflation Hedge Question

A Gold ETF’s NAV tracks the domestic gold price. That price is international spot gold in dollars multiplied by the USD/INR rate, plus import duty and GST. So your return has two engines: the global gold price and the rupee’s movement against the dollar.

This is the double-edged currency risk. When the rupee weakens, the NAV gets a tailwind. Your ETF can rise even if international gold is flat. But when the rupee strengthens, that same mechanism works against you. A 5% rupee appreciation can erase a 5% gold rally and leave you with nothing.

Does a Gold ETF hedge domestic inflation? Conditionally. Over multi-year periods, gold has tended to preserve purchasing power in rupee terms. But the lag can be long and uneven. A sharp inflation spike does not guarantee an immediate NAV jump. Treat the ETF as a partial, slow-moving hedge, not a real-time inflation shield.

Monitor USD/INR trends alongside international gold prices. If you ignore the currency leg, you are reading only half the chart.

Tracking Error: Why Your Fund Returns Lag the Metal

Even a well-run Gold ETF will return slightly less than the physical metal it tracks. That gap is tracking error. It is not a malfunction. It is the silent arithmetic of fund operation.

Three sources dominate.

Cash drag: the fund holds a small cash buffer for expenses and redemptions, and that cash earns nothing close to gold’s return. Expense accrual: the expense ratio is deducted from the NAV daily, not once a year, so it compounds against you. Timing mismatches: when Authorized Participants create or redeem large creation units, the fund’s gold position can lag the index for a few hours, and that tiny gap adds up.

You can spot tracking error in a fund’s monthly factsheet. Look for the one-year return difference between the ETF’s NAV and the domestic gold price benchmark. A gap of 0.5% to 1.2% is common.

It varies across fund houses because cash management and creation-unit efficiency differ. A fund with a low expense ratio can still have high tracking error if its cash drag is sloppy.

The Liquidity Trap: Low Volumes and Wide Bid-Ask Spreads

AUM is the number fund houses flaunt. It tells you how much gold the fund holds. It does not tell you how easily you can get out. For that, you need average daily traded volume.

A large AUM ETF can trade surprisingly little, while a smaller one can be far more liquid. For example, a ₹2,000 crore AUM ETF might trade only a few lakh rupees a day, while a ₹500 crore AUM ETF could trade several crore.

When volume is thin, the bid-ask spread widens. On a volatile day, you might pay 0.5% or more just to enter or exit, before brokerage. That spread is an immediate, unrecoverable cost.

Check average daily traded volume before selecting an ETF. Rank the counters by three-month average volume, not by AUM. If you cannot find a counter that trades at least a few crore rupees daily, accept that your intraday liquidity benefit is mostly theoretical.

Knowing the risks sets your filter. Now you need a systematic way to evaluate any Gold ETF against measurable benchmarks.

How to Evaluate and Select a Gold ETF: Metrics That Matter

You now know what can go wrong. The next step is building a screening framework that catches those problems before your money is in the trade. Most investors stop at the expense ratio. That is a mistake. A Gold ETF’s true cost has three layers, and you need to read all of them like an analyst, not a brochure-browser.

Expense Ratio and Tracking Error: Reading the Factsheet Like an Analyst

The expense ratio is the visible annual fee, ranging from roughly 0.29% to 0.80% for Indian Gold ETFs. A lower number looks better. But the expense ratio is only half the cost story. Tracking error is the hidden performance drag. It measures how much the fund’s NAV return lags the domestic physical gold price return, after fees.

A fund can advertise a 0.29% expense ratio and still deliver a 0.50% tracking error because of cash drag, imperfect replication, or management inefficiencies. That gap eats your returns silently.

| EXPERT TIP: Always cross-check the fund’s AMFI monthly factsheet for tracking error. A 0.29% expense ratio fund with 0.50% tracking error costs more in real terms than a 0.50% expense ratio fund with 0.10% tracking error. |

You find tracking error data in the fund’s factsheet and the AMFI monthly reports. Ignore any fund that does not disclose it clearly. The analyst-grade filter is simple: add the expense ratio and the tracking error. That sum is your annual performance leakage. Pick the fund with the smallest total leakage, not the smallest headline fee.

Liquidity Benchmarks: Volume, Impact Cost, and AUM

AUM size is a comfort blanket. It tells you the fund is popular, but it does not tell you whether you can exit at a fair price. Liquidity lives on the exchange, in the daily traded volume and the bid-ask spread. A fund with ₹10,000 crore AUM can still trade only a few lakh rupees a day.

When you place a market order in that thin counter, the price moves against you. That movement is impact cost.

A healthy retail liquidity benchmark: average daily traded volume above roughly ₹5 crore, and a bid-ask spread consistently under 0.15% (as a rule of thumb). Check the spread on the NSE or BSE website before you buy, not after.

Authorized Participants (APs) are the market makers who create and redeem units. Active APs keep the spread tight. A fund with dormant APs will have a wide, sticky spread that punishes every entry and exit.

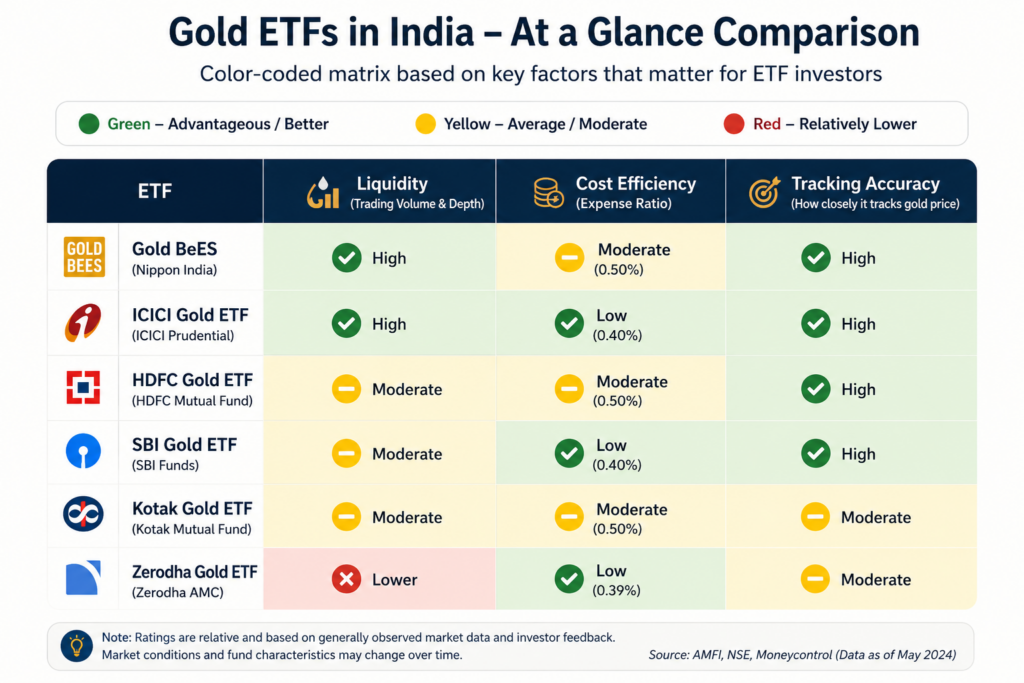

The Gold ETF Health Scorecard: A Visual Rating System

| Gold ETF Health Scorecard To make ETF selection easier, I created a simple Gold ETF Health Scorecard that evaluates each fund across three practical factors: Liquidity – How easily the ETF can be bought or sold without a large bid-ask spread. Cost Efficiency – The overall cost of holding the ETF, including the expense ratio. Tracking Accuracy – How closely the ETF follows the price of physical gold. Rather than focusing on a single metric, the scorecard provides an at-a-glance comparison using a simple colour-coded matrix. This helps investors quickly identify funds that balance liquidity, low costs, and consistent tracking performance. |

The scorecard forces you to weigh all three dimensions together. A fund that scores green on cost but red on liquidity is a trap. A fund with moderate cost and green tracking accuracy often wins over a cheap fund that leaks through tracking error. Use this visual filter before you even look at the fund name.

Practical Screening Checklist Before You Buy

Run this five-point check before you place a single order:

1. Pull the latest AMFI factsheet. Confirm the expense ratio and the one-year tracking error. Reject any fund with a combined leakage above roughly 0.70%.

2. Check the NSE/BSE snap quote for the current bid-ask spread. If the spread is wider than roughly 0.20%, walk away or use a limit order.

3. Verify AP activity. The factsheet lists the APs. A fund with only one or two inactive APs is a liquidity risk.

4. Cap your total gold allocation at 5–10% of your portfolio. Gold is a hedge, not a growth engine.

5. Always use a limit order. Place your buy limit at the mid-point of the bid-ask spread to avoid paying the full spread.

Even the best fund pick is worthless if the tax treatment blindsides you at filing time. The regulatory and taxation framework is your next required reading.

Taxation and Regulatory Framework: What SEBI Rules Mean for Your Returns

Gold ETFs are taxed based on your holding period.If sold within 12 months, gains are taxed as per your income tax slab.

If held for more than 12 months, gains qualify for long-term capital gains tax at the applicable rate. Since tax rules can change, always check the latest regulations or consult a tax professional.

STCG and LTCG: Holding Periods and Rates for Gold ETFs

The line is now 12 months. Hold your Gold ETF units for more than 12 months, and the gain qualifies as long-term capital gains (LTCG), taxed at a flat 12.5% with no indexation benefit. Sell within 12 months, and the gain is short-term capital gains (STCG), added to your income and taxed at your slab rate, which can push the effective rate well past 30% for top-bracket investors.

This is a sharper bite than physical gold, where the LTCG threshold remains 24 months as of publication. An ETF holder who exits at month 13 pays 12.5% on the entire gain. A physical gold holder selling at the same point pays slab-rate STCG. The ETF’s liquidity advantage comes with a tax clock that runs faster. Before April 2025, Gold ETF LTCG was 20% with indexation, which often reduced the taxable gain materially. That cushion is gone.

Indexation Benefits and Tax-Efficient Alternatives

Indexation is no longer available for Gold ETFs under the April 2025 regime. Units bought before that date still qualify for the old 20%-with-indexation rule on sale, but that window closes as holdings age. Fresh purchases face the 12.5% flat rate as the only path.

SGBs retain a structural tax edge that no ETF can match. If you hold an SGB until its 8-year maturity, the redemption proceeds are entirely exempt from capital gains tax. That zero-tax exit makes SGBs the most tax-efficient gold instrument for long-term holders who can lock in the tenor.

The trade-off is liquidity. SGBs trade on exchanges but often at a discount, and the secondary market is thin. For an investor with a genuine 8-year horizon, the post-tax return gap between an SGB and a Gold ETF can be substantial. The zero-tax exit at maturity is the decisive edge.

| Note: Tax rules and regulations can change over time. Always refer to the latest Income Tax Department, SEBI, or AMFI guidance before making investment decisions. |

Tax efficiency and regulatory safety are defensive layers. Now we turn to offence: how to build a gold allocation strategy that responds to your life and the macro environment.

| Some investors also use Gold ETFs to gradually build a gold allocation for long-term goals such as weddings, education expenses, or wealth preservation. Unlike jewellery, Gold ETFs do not involve making charges, storage concerns, or purity issues. This allows investors to accumulate gold exposure over time while maintaining flexibility and transparency. When the funds are needed, the ETF units can be sold on the exchange, making them a convenient alternative to accumulating physical gold for future financial goals. |

This reframing matters. The cultural saver often fears that digital gold lacks the tangibility of jewellery. But a regulated ETF unit, backed by physical gold of 995 fineness held in SEBI-audited vaults, is more tangible in purity terms than most hallmarked jewellery. The emotional loss is a perception gap, not a real one.

Rebalancing Discipline and Systematic Accumulation

Gold’s low correlation with equity means its portfolio weight drifts significantly during bull and bear cycles. Annual rebalancing (selling down the overweight asset and topping up the underweight one) restores your intended risk profile. It also forces you to buy gold when it is cheap and trim it when it is dear, a discipline most investors abandon in euphoria or panic.

But do not over-trade. STCG tax and brokerage can destroy the ETF’s cost advantage over physical gold.

A Gold ETF held for less than 12 months attracts short-term capital gains at your slab rate. Add brokerage on each buy and sell leg, and frequent tactical shifts quickly erode the expense-ratio savings you thought you were capturing. Treat your Gold ETF position as a strategic allocation, not a trading vehicle.

For systematic accumulation without a demat account, Gold Fund of Funds (FoFs) offer SIP routes that enforce discipline. They carry an additional layer of expense, but the behavioural benefit of automated, regular investing often outweighs the cost for savers who would otherwise time the market poorly.

Strategy without instrument selection is incomplete. Here are the specific funds and screening tools that deserve your attention.

Recommended Gold ETFs and Essential Screening Tools

You have the framework, the cost model, and the strategy. Now you need the names and the numbers: the actual funds and the tools to verify them.

Curated Fund Overview: India’s Liquid and Cost-Efficient Options

Six Gold ETFs dominate the Indian market in liquidity and cost efficiency. Their expense ratios and AUM shift quarterly, so treat every number as a snapshot, not a promise.

The Nippon India ETF Gold BeES remains the largest by AUM and daily traded volume. That deep order book keeps impact cost low, though its expense ratio sits above newer disruptors.

Roughly ₹8,770 Cr in AUM backs the ICICI Prudential Gold ETF. It charges a 0.50% expense ratio and has delivered a 0.22% tracking error, a tight spread between NAV and physical gold.

HDFC Gold ETF carries a 0.59% expense ratio. SBI Gold ETF runs slightly higher, around 0.64–0.65%. Both offer adequate liquidity for retail-sized orders.

Mid-range cost and volume define the Kotak Gold ETF, a steady option without headline-grabbing extremes.

Disruption arrived with the Zerodha Gold ETF (ZGOLD) and its razor-thin expense ratio. But liquidity is the hidden cost driver. A fund with a 0.30% TER and negligible daily volume can cost you more in impact cost than a 0.59% TER fund with deep order books. The spread widens when you need to exit. That erosion never appears in the TER.

Using AMFI and Moneycontrol Screeners Effectively

AMFI’s mutual fund screener and Moneycontrol’s ETF tools are free and powerful, if you know their blind spots. Both rely on monthly disclosures. A fund’s expense ratio can change mid-quarter, and a merged scheme or renamed ticker can leave stale data in the screener for weeks.

Start with the expense ratio filter, then manually check the “Average Daily Volume” column. A fund with 0.30% TER but negligible volume is a trap. Low volume means a wide bid-ask spread and a higher impact cost when you buy or sell more than a few units. Cross-check tracking error against the fund’s latest factsheet. Screeners often lag by a month.

Red flags: a ticker that suddenly shows zero volume, a scheme that has been merged into another, or an expense ratio that looks too good to be true. Always verify against the AMC’s own factsheet PDF.

Note on Data Freshness and Verification

Expense ratios, daily volumes, and taxation rules change. The numbers in this section were verified against AMFI disclosures and fund factsheets immediately before publication. We commit to quarterly updates, but you should treat every figure as a checkpoint, not a permanent truth. Before you act, open the latest factsheet and confirm the TER and tracking error yourself.

Data ages. The final section is your decision checklist and your next action.

Conclusion

You’ve audited the costs, compared the alternatives, and screened the funds. The only question left is: should you buy, and if so, what do you do tomorrow morning?

The answer hinges on three numbers: your total cost of ownership, your holding period, and your access to alternatives. If you already have a demat account and you’re parking money for six months to three years, a low-TER Gold ETF is the cleanest, most transparent gold vehicle available. SEBI oversight, real-time NAV, and exchange liquidity give you a level of price discovery that physical gold and digital gold can’t match.

But if your total annual cost (expense ratio + brokerage + demat AMC) crosses 1.5%, the math flips. Physical gold or a gold FoF may be cheaper. Run the numbers from the cost comparison section before you commit.

Who Should Own a Gold ETF, and Who Shouldn’t

A Gold ETF fits you if you hold a demat account, need short-to-medium-term liquidity, and want a SEBI-regulated product where the price you see is the price you get. It’s the right tool for tactical allocation, portfolio rebalancing, and systematic accumulation without the making charges and purity risk of jewellery.

It’s the wrong tool if you’re chasing long-term tax-free gold returns. Sovereign Gold Bonds historically won that race, but new issuances are paused. If you can’t tolerate any brokerage drag or demat AMC, a gold FoF or even physical gold held in a locker may suit you better. The ETF’s transparency comes with a small recurring cost. Accept it or choose a different vehicle.

Your Next Move: Account Opening, Rebalancing, or Switching

Stop analysing. Start acting.

No demat and trading account? Open one. A basic account with a discount broker takes a morning. Without it, you’re locked out of the entire ETF universe.

Already holding Gold ETFs? Review your current allocation. Check whether your fund’s tracking error has drifted. Compare it against the health scorecard from the screening section. A fund that consistently lags its benchmark by more than 0.5% is quietly eroding your returns.

Holding physical gold, digital gold, or an expensive FoF? Run the cost comparison. Switching to a low-TER ETF could save you hundreds of basis points a year. Before your next purchase, pull up the AMFI screener, check the latest expense ratio and daily volume, and place your order. The market opens tomorrow.

FAQ

What is the real annual cost of owning a Gold ETF in India?

Beyond the advertised expense ratio (0.40%–0.50%), you pay brokerage, demat AMC, GST on trades, and impact cost from bid-ask spreads. The total can exceed 1.5% annually, especially for small holdings.

How does a Gold ETF compare to Sovereign Gold Bonds (SGBs)?

SGBs offer tax-free redemption after 8 years, making them more tax-efficient for long-term holders. However, fresh issuances are currently suspended. Gold ETFs provide intraday liquidity but are taxed at 12.5% LTCG after 12 months with no indexation benefit.

Do I need a demat account to invest in Gold ETFs?

Yes, direct Gold ETFs require a demat and trading account. If you don’t have one, you can use Gold Fund of Funds (FoFs) which don’t need a demat but charge an additional layer of expense ratio, making them costlier over time.

What is tracking error and why does it matter?

Tracking error is the gap between the ETF’s NAV return and the domestic physical gold price return. A fund with a low expense ratio can still have high tracking error due to cash drag or inefficiencies. Always check the AMFI factsheet and add expense ratio + tracking error to find the true annual performance leakage.

How do I check liquidity before buying a Gold ETF?

Look at average daily traded volume and the bid-ask spread on NSE/BSE, not just AUM. A fund with large AUM can be illiquid. Use limit orders and avoid counters where the spread exceeds 0.20% or daily volume is below roughly ₹5 crore.

Are digital gold platforms safe?

Digital gold platforms operate in a regulatory grey zone with no statutory backing for investor claims. They embed a 2–5% buy-sell spread and lack SEBI oversight. Gold ETFs, by contrast, hold physical gold in SEBI-approved vaults with independent audits and insurance.